In recent weeks, a range of ideas and narratives have circulated across the market aimed at addressing challenges in the housing sector—particularly those tied to Agency mortgage-backed securities (“MBS”). This commentary outlines our perspective on the key policy proposals currently under discussion and offers a framework for evaluating their potential impact on the MBS market. We also highlight concerns around the possible transfer of risk to taxpayers, which we believe warrants careful consideration in any proposed solution.

1. Agency MBS Spreads Are Very Tight and Have Room to Widen

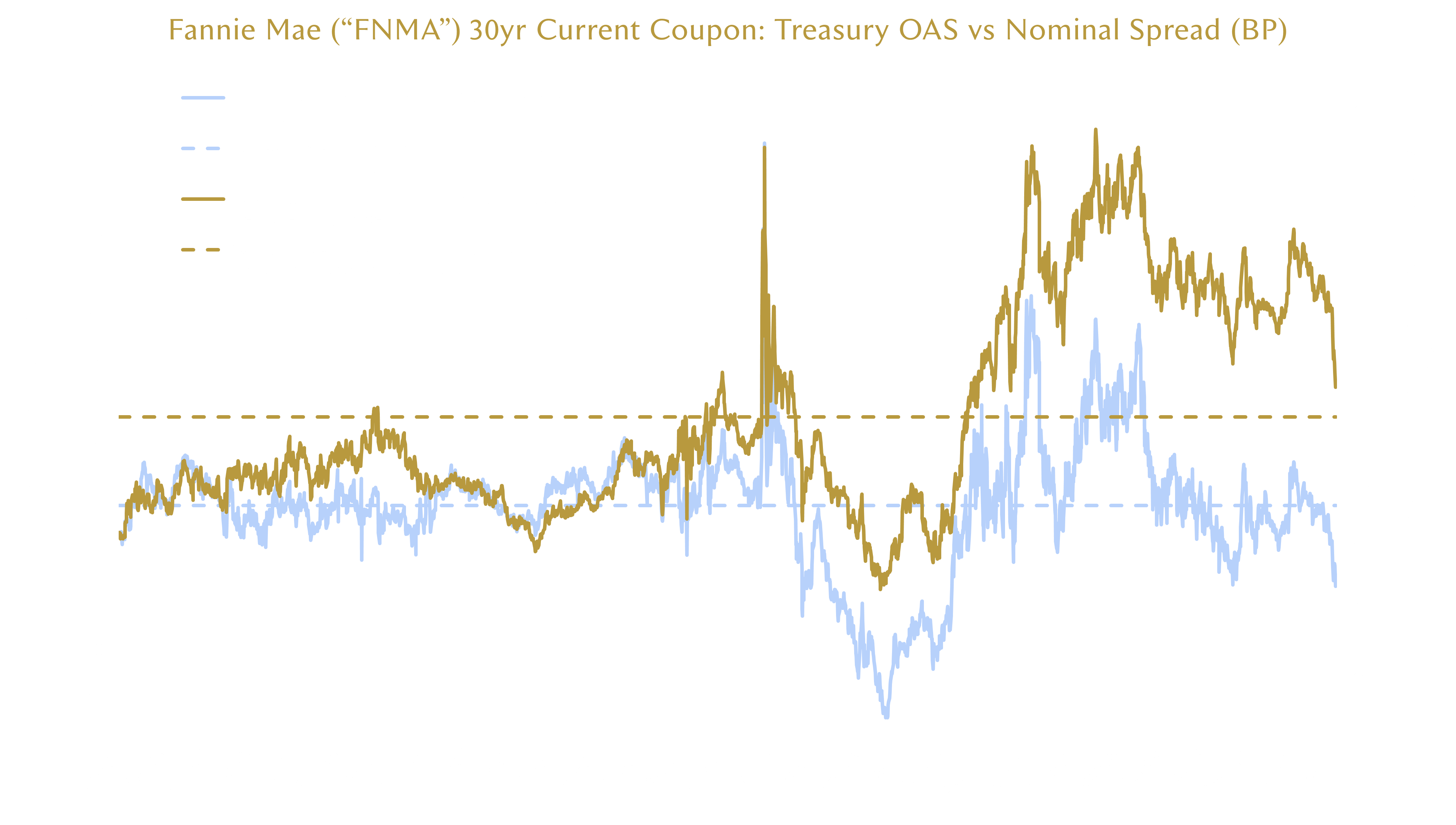

Since late July, nominal MBS spreads have tightened significantly—from approximately 150 basis points (“bp”) over the 7-year U.S. Treasury to around 120 bp by mid-September. This marks the tightest level since 2022, but as many with longer perspectives have recently pointed out, still significantly wider than the 82 bp average from 2013-2019. These participants have been searching for potential paths in which Agency MBS return to the extremely narrow pre-COVID levels (when the Federal Reserve (“Fed”) was buying hundreds of billions of MBS every year as part of QE), throwing around many forms of government support as a potential mechanism. However, we think this view ignores the obvious reality that borrowers are currently significantly more efficient at exercising their prepayment option than they were before COVID, which means today’s 120 bp is more expensive, in our opinion, than 82 bp was back then.

The more appropriate measure to account for borrower behavior is Option-Adjusted Spread (“OAS”), which reduces the nominal spread by the expected cost to hedge prepayments and volatility risk. Similar to a loss-adjusted spread in credit, OAS provides a more comprehensive, hedge-adjusted perspective of the excess return. Viewed through this lens—as illustrated in the chart below—OAS are approaching their lowest levels since 2013 and are hovering nearing zero! In this context, further meaningful tightening appears unlikely, and even if spreads widen beyond the current 120 bp, they would still fall within a historically normal range.

2. Lower Rates Can Induce Large MBS Buying

As a reminder, the Agency MBS market is the second largest global fixed income market next to U.S. Treasuries with over $9T outstanding and ~300B traded daily on average. The main participants are gargantuan in size and include Money Managers, Commercial Banks, Overseas investors, and Mortgage REITs; when they adjust their massive MBS portfolios to account for shifting rates and duration, the impact on spreads can be quite consequential.

Specifically, when Treasury rates fall as they have in recent weeks, a phenomenon known as “convexity buying” occurs (please stay with us here, it’s worth it). What this means is that as interest rates decline, the duration of MBS shortens given that more underlying borrowers are expected to utilize their prepayment option. Many MBS holders are seeking a constant duration and thus must purchase more MBS to essentially replace those that are likely to prepay. These purchases can be enormous and temporarily drive spread tightening. At the same time, rates are always shifting, which means this effect is typically short-lived. Eventually, we anticipate one of three outcomes will occur to remedy this situation:

Rates rise which triggers a reversal of all that convexity buying into convexity selling, which leads to a widening of spreads.

Lower mortgage rates spur increased originations, boosting MBS supply, which typically pressures spreads wider.

Rates remain constant, and new, longer duration MBS are created (as the prepaying borrowers take out new mortgages), which the market absorbs, but at a more normal (cheaper) valuation level.

3. Policy Speculation and Potential Market Impact

Recent spread compression has coincided with speculation that the administration may intervene to lower mortgage rates by narrowing MBS spreads relative to Treasuries. While well-intentioned, we believe such efforts would be misguided, especially given where spreads currently reside.

Two mechanisms have been floated:

A. FNMA & Freddie Mac (“FHLMC”) Allowed to Expand Retained Portfolios and Buy Agency MBS

While this could theoretically reduce mortgage rates, we see two major concerns:

Elevated Risk for Taxpayers:

The GSEs required taxpayer bailouts in 2008 due to excessive portfolio exposure. Re-engaging them as large-scale buyers could reintroduce systemic risk especially if the government pressures them to buy MBS at uneconomic levels. Taxpayers should be concerned if FNMA and FHLMC are encouraged to turn back into the de facto hedge funds they once were.

Poor Spread Economics (currently):

Based on the Yield Book and OASIS models, par coupon MBS currently offer Treasury OAS of just 5–18 bp. With FNMA/FHLMC debt trading at Treasuries +3–20 bp, buying MBS at these levels would likely be unprofitable and eventually stick the entities with losses. However, we concede that if it is the case that FNMA/FHLMC are patient and buy MBS at wider levels, this could be beneficial for them and help reduce upticks in mortgage rates during times of economic stress.

B. Federal Reserve Comes Back to Buy Agency MBS

Two Fed-related ideas have recently surfaced, both of which raise significant concerns in our view:

Reinvesting MBS Runoff:

While this approach could compress spreads, it would effectively position the Fed as a buyer of last resort—or a “garbage bin”—for par coupon MBS. In practice, this would enable market participants to offload less desirable securities to the Fed, shifting risk to taxpayers and facilitating portfolio rebalancing for current holders. We view this as a misallocation of public resources and an inefficient use of the Fed’s balance sheet. Notably, with Money Managers having shifted from a significant underweight to a meaningful overweight in MBS over the past few years, there’s a high likelihood that Fed purchases would serve more as an outlet for repositioning existing holders than as a catalyst for tighter spreads or lower mortgage rates.

“Operation Twist”:

This proposal is even more problematic. Historically, Operation Twist has involved the Fed selling higher-coupon short duration MBS to buy lower-coupon longer duration MBS. The current suggestion some mortgage buyers have promoted is that the Fed should sell its existing long duration 2.0%, 2.5% and 3.0% coupon MBS to buy shorter par coupon MBS. This introduces new risk. If the buyers of the Fed’s MBS sales need to maintain neutral mortgage exposure, they may need to sell even more par coupon MBS, potentially leading to wider spreads and higher mortgage rates. For knowledgeable market participants to suggest this strategy would not risk producing higher rates seems, at best, disingenuous. We believe selling net mortgage duration is an extremely counterproductive move if the Government’s goal is to lower mortgage rates and stimulate housing.

Given the Fed’s stated reluctance to favor specific sectors, with most Fed Governors more recently discussing when they would outright sell their MBS portfolios to reinvest into UST, we find the discussion around the Fed surprising. Furthermore, the absence of crisis-level spreads today (we argue spreads are actually too tight) makes the discussion around using Federal Reserve balance sheet to reinvest into more MBS antithetical to the stated goals. That is why we believe both above options should remain off the table with Agency MBS, especially given where current spreads are situated.

4. Structural Considerations

Despite nominal spreads at 120 bp, which is still above the 2013–2022 average, OAS remains compressed (depending on your model only earning 5-18 bp more than Treasuries after hedging costs) due to increased borrower efficiency in refinancing. While this is positive for homeowners, it presents valuation challenges for bondholders, who must price in higher prepayment risk. This increased borrower efficiency is a structural change which is likely to keep MBS spreads wider to Treasuries than in the past, leading to higher mortgage rates. In essence, the benefit of more borrowers refinancing to lower rates isn’t free, and mortgage rates unfortunately had to rise to price in that risk.

5. Conclusion

At current spread levels, policymakers should be encouraged that the MBS market can function normally without Fed manipulation. Despite Quantitative Tightening, Agency MBS OAS remain near historic lows. Mortgage rates can still decline via falling Treasury yields but further spread compression would likely require taxpayer risk—an outcome we believe could be dangerous and should be avoided.

*Sources: JP Morgan Markets, Yield Book, Bright Meadow Team property analytics. OAS accounts for the cost of hedging negative convexity of Agency MBS and is a more accurate measure of MBS spreads in our opinion. Refers to the Team’s proprietary OAS analysis, which is based on the Bright Meadow Team’s modelling and proprietary analysis and Yield Book and is based upon interest rate volatility and prepayment speed assumptions among others. There is no guarantee that the Bright Meadow Team’s assumptions will reflect actual market conditions, and this example should not be relied upon for any investment decision.